When it comes to life insurance, the number one question many people ask is, “Do insurance companies really pay claims?”

This is because the insurance world isn’t straightforward, especially when it comes to getting a claim paid.

Different insurance companies have distinct terms, conditions, and definitions that can be confusing to someone with little to no knowledge of how insurance works.

Total and Permanent Disability (TPD) insurance is one of the more complex products on the market, particularly when it comes to making a successful claim.

Since TPD insurance claims are complex, we review the statistics around them to offer readers an expert analysis of the average acceptance rate of TPD claims in Australia.

Key Takeaways

- According to data from the Australian Securities and Investments Commission (ASIC) and the Australian Prudential Regulation Authority (APRA), the country’s life insurance industry pays more than 90% of people’s claims.

- The total percentage of claims paid between 2016 and 2021 ranged from 92% to 94%.

- Mental health illness and injury or fracture are the diseases with the highest claims decline rate in Australia.

- Resolution Life/AMP had the highest TPD claims acceptance rate of 93.6%, while AIA had the lowest.

- The TPD and Disability Income Insurance (DII) shot up in December 2020 but returned to a lower 70% to 80%

TPD Insurance Claims Statistics

According to research, the average TPD claims statistics for the entire Australian life insurance industry was 86.8% in 2021.

However, data from APRA and ASIC states that the overall percentage of claims paid by all life insurance providers between 2016 and 2021 was 92% to 94%.

The percentage of claims paid by the life insurers cut across varying insurance types, but life insurance and income protection insurance claims had the largest share.

Both claims amounts were significantly higher than what was paid for TPD and Trauma claims during the same period.

Additionally, ASIC stated that the direct life insurance payout ratio was significantly lower than the advised segment of the market (where we operate).

The research cited issues like high cancellation rates and unsuccessful claims, suggesting that companies are selling insurance products customers don’t want, can’t afford, or don’t consider right.

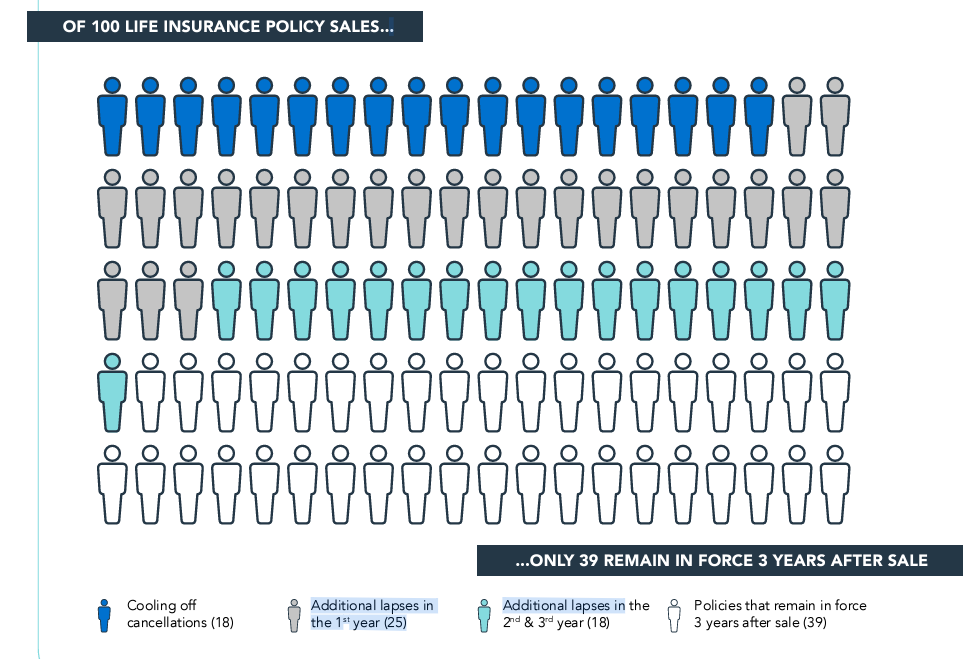

As shown in the infographics below, of every 100 life insurance policy sales, only 39 remain in force after the first three years.

Source: ASIC Claims Statistics

At the same time, ASIC discovered that customers frequently experienced poor service from the insurance providers, resulting in poor customer outcomes within the period.

Source: ASIC Claims Statistics

In summary, insurers still have room for improvement to ensure customers get what they need and enjoy the best experience to turn around the unimpressive payout ratio as far as life insurance policy sales are concerned.

Average TPD Claims Acceptance Rate

The average TPD acceptance rate from life insurance companies in 2021 was 86.8%.

But more recent research showed that the industry’s average acceptance rate for TPD claims grew to 93.6% in 2022, a significant jump within a one-year period.

The average claim time for a TPD insurance claim acceptance in 2022 was 7.5 months. Among all the insurers during the period, TAL/Asteron was the fastest TPD claim provider, with an average processing time of 6.2 months.

Conversely, the slowest TPD insurer was Zurich/OnePath, with an average claims processing time of 8.8 months.

Additionally, the report shows that the admittance rate for all insurance cover types has been relatively stable between 2021 and 2022.

However, data from APRA and ASIC shows that the industry’s claims acceptance rate has improved, with TPD claims acceptance rates increasing from 86.6% to 86.8% over a 5-year period from 2018 to 2022.

Percentage of TPD Claims Paid Overall

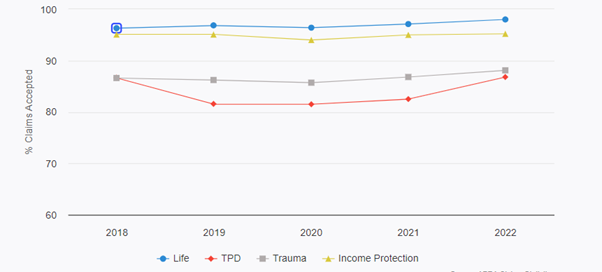

From 2018 to 2022, APRA and ASIC state that life insurance claims among insurers increased from 96.3% to 98%. During this period, the TPD claims acceptance rate experienced a resurgence that moved it from 86.6% to 86.8%.

Trauma claims acceptance rates also increased from 86.6% to 88.1%, while income protection insurance claims acceptance rates experienced little growth from 95.1% to 95.2%.

When looking at the life insurance industry holistically, TPD insurance claims have been rising and falling, but their acceptance rates continue to hover between the 80% and 90% mark. On the other hand, the income protection insurance acceptance claim rate remains steady at around 95%.

Percentage of Life Insurance claims accepted by AU insurers. Source: APRA Claims Statistics

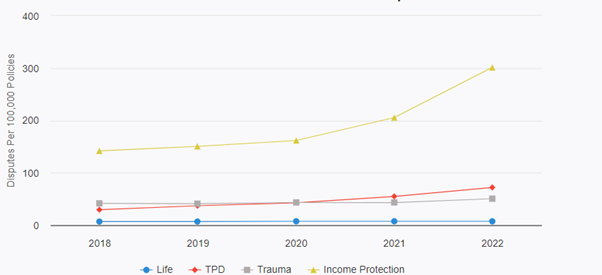

However, on the downside, the same period has seen a significant increase in claims disputes across all product categories in the life insurance space, including TPD insurance. The high dispute rate is directly in tune with the overall number of claims.

For example, APRA statistics show that the significant increase in income protection claims has been matched by a high income protection claims dispute rate.

However, the TPD claims dispute rates have been relatively steady within the four-year period, with less than 100 disputes, as shown in the infographics below.

Claim Disputes in the Life Insurance Sector. Source: APRA Statistics

Average time for a TPD claim to be accepted

In 2022, the average time for a TPD insurance claim to go through was 7.5 months, and the overall industry average acceptance rate was 86.8%.

Resolution Life/AMP had the highest TPD claims acceptance rate of 93.6%. That means less than 1 of every 10 claims were not accepted by the insurer.

AIA had the lowest claims acceptance rate of 77.8%, representing nearly 8 out of 10 successful TPD insurance claims from the life insurer.

In terms of claim acceptance speed, TAL/Asteron was the fastest, with an average TPD claims acceptance transaction time of 6.2 months, and Zurich/OnePath had the slowest transaction time of 8.8 months.

Declined TPD claim rates

While there were decent claims acceptance rates by super insurers, some life insurance companies like Asteron had a high refusal rate per claim, up to 29%.

That means Asteron did not pay almost every 30 out of 100 TPD claims it got.

TPD claim withdrawals accounted for 81% of the total life insurance industry refusals.

The major reasons for withdrawal included customers’ decisions to withdraw, refusals because some consumers were returning to work, and lack of response to an information request.

The medical conditions that were declined the most include mental health and musculoskeletal illnesses. Typically, your claim is highly prone to a decline with these kinds of illnesses, as they may not be considered as complete and permanent disabilities by insurers.

For example, statistics show that TPD claims for mental health illness and fracture claims had the highest decline rates of 16.9% and 16.1%, respectively.

Conversely, claims for disease-related challenges had a decline rate of 9.7%, which is relatively lower.

Distribution channels like direct policies, retail policies, and group policies also had the highest decline rates.

However, It is important to note that the overall approval or refusal rate does not represent whether a superannuation insurer is good or bad.

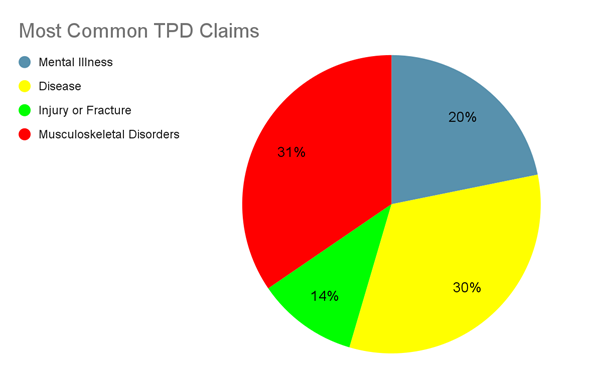

What are the most common TPD claims?

You can make a TPD claim if you’re injured or ill and unable to work.

However, some illnesses are more common than others. The pie chart above shows the most common reasons for TPD claims in Australia.

- 31% of TPD claims in Australia are made by people with Musculoskeletal disorders, making it the most common medical challenge in the country.

- Diseases account for 30% of the total TPD claims.

- Mental health illness is the third most common reason for TPD claims, with 20% of the total claims. Popular examples include Post Traumatic Stress Disorder (PTSD), severe depression, schizophrenia, and personality disorders.

- Injury and fracture account for 14% of the claims.

- The remaining 5% is for other categories of medical conditions.

Want to Maximise Your Chances of Getting Your TPD Claim Approved?

The current TPD claims acceptance rate in Australia is quite high.

However, some insurers still decline claims for many reasons. If your TPD claim gets declined by an insurer, it’s crucial to understand that a declined claim does not mean the end of your claims process or indicate that you will never get a TPD payout in the future.

If your TPD claim is declined, you can submit a formal complaint for the life insurance company to review your application and reconsider its initial decision.

Sometimes, an appeal may result in a successful claim however this may be a difficult process in the absence of

However, if you want to brace yourself for the appeal, you can contact our TPD claims experts.

Our financial advisers have a solid track record of helping TPD claimants get their due entitlements and can review your refusal to provide all the legal advice you need to challenge your initial TPD claim refusal.

Contact us today to get started!

General Advice Disclaimer: The advice provided is general advice only and in preparing it we did not take into account your investment objectives, financial situation or particular needs. Before making an investment decision on the basis of this advice, you should consider how appropriate the advice is to your particular investment needs, and objectives. You should also consider the relevant Product Disclosure Statement before making any decision relating to a financial product.