How to Deal with a Rejected Trauma Claim?

As with all Life Insurance claims, you have the right to appeal a claims decision and have it reviewed. We managed many claims where it was initially declined only to be later approved. There are a number of reasons why this might happen which is why it is crucial to have an expert on your side to ensure the process goes as smoothly as possible. If you feel your claim has been assessed unfairly, speak with us to see if we can assist.

Is a Trauma Insurance Payout Taxable?

Generally no tax is payable on trauma insurance payouts. Typically tax will only be payable should the policy be held for business purposes where CGT tax may apply. As a result of this, Trauma Insurance premiums are also generally not tax deductible.

How Much Will I Receive from my Trauma Insurance Claim?

The amount you will receive from a Trauma Insurance claim is determined byt he the benefit you are insured for. Generally this amount is agreed upon at the start of the policy and is reviewed as time goes by. More comprehensive Trauma Insurance Policies have both full and partial payout. A full payout refers to when you are eligible to claim the entirety of the amount you are insured for while partial payments are for ‘less serious’ trauma’s where only a fixed percentage of your benefit is paid out. When you have received a partial payment under your trauma contract, you may well be entitled to retain the remaining portion of your benefit for future claims. However, your benefit will likely reduce by the amount that you have already claimed.

How Long Will My Trauma Insurance Claim Take To Be Paid?

If handled correctly, a trauma insurance claim can be settled within a few days of the appropriate paperwork being submitted. However, if you do not understand the process intimately and have experience in anticipating further requirements from the insurer, these payments can be delayed for a number of months. Trauma claims are seldom as simple as they seem which is why it is vital to engage the services of a professional prior to putting your forms together.

When can you claim Trauma Insurance?

Trauma insurance is payable upon meeting the definition provided in your policy document. As mentioned previously, many definitions contain waiting periods which might make you ineligible for a payment should you fall ill within a certain time of the policy starting. More comprehensive insurance products contain clauses that allow for discretion to be applied by the claims assessor should your illness not fall within the specific parameters provided by the insurer. For example, your cardiologist might advise you that you have had a heart attack without meeting the traditional criteria such as raised markers in your blood test. These clauses provide greater scope for the insurer to act in good faith and allow their medical definitions to remain dynamic and up to date.

Can I get Trauma Insurance Again After I Have Claimed?

You can often apply for the reinstatement of your Trauma policy once a claim has been paid. This is a feature of the product and is not standard amongst insurers. Generally, you will be required to wait 12 months before your benefit can be reinstated. Further, you will generally not be covered for the same medical condition that you previously claimed, preventing you from being able to have two bites of the cherry.

Does Trauma Insurance Cover Death?

Although Trauma Insurance is often linked to life insurance, Trauma Insurance is not designed to payout in the event of death. Some Trauma Insurance contracts include a small benefit that is payable in the event of death and is often capped at an amount of $10,000.

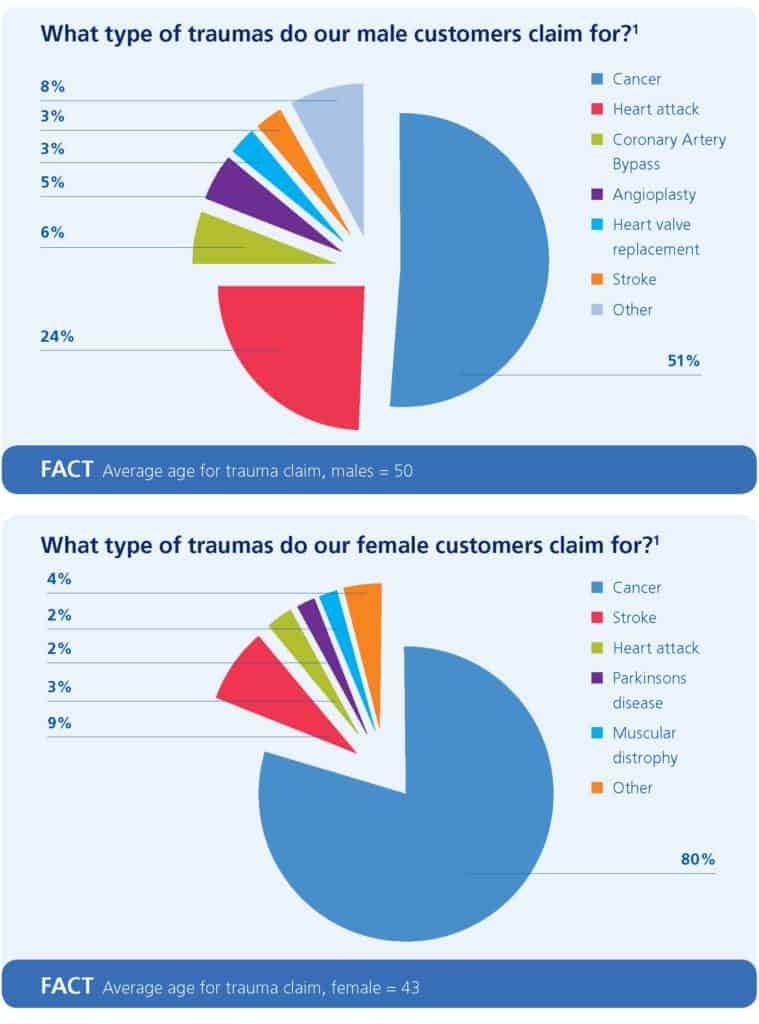

What are the Most Common Causes of Trauma Insurance Claims?

Although these statistics are hard to compile due to privacy restrictions that are inherently associated with such sensitive data, Zurich Life has advised that in 2014 the most common reason for a Trauma claim were:

Males

- Cancer – 51%

- Heart attack – 24%

- Heart bypass – 6%

- Angioplasty – 5%

- Stroke – 3%

Females

- Cancer – 80%

- Stroke – 9%

- Heart attack – 3%

- Parkinson’s disease – 2%

- Muscular distrophy – 2%

Source: Zurich